For the past 7 years that I’ve been tracking the growth of the marketing technology landscape, I’ve been hearing prophecies of its consolidation.

I’ve been quick to acknowledge that’s a possibility, probably an inevitable one. In fact, if you look at the distribution of revenue across martech companies today, you can argue it’s already happened. But I’ve found it ironically amusing that, at least in the short term, the more predictions of consolidation there have been, the larger the landscape has grown.

My meta-level takeaway: predicting the future in a complex environment is hard. That’s why I feel much safer playing the role of the empiricist — describing what’s actually happening today — than the prophet claiming to know what will happen tomorrow. And it’s why I encourage marketers to think in terms of optionality for their own marketing stacks.

But there is a case for a coming “martech apocalypse” that I’ve heard from multiple sources — primarily people in corporate development who look at the martech landscape as a kind of M&A buffet — that I think could dramatically change the dynamics in this space.

But not necessarily in the way they think it will.

The Devil Went Down to Georgia Tech

The premise is this: there are a significant number of martech companies that have taken large amounts of VC funding, their burn rate is much greater than their revenue, and the exponential growth curve that their VCs expected of them is flattening out.

It’s important to note — and we’ll come back to this — that many of them are great companies, with amazing products and happy customers, continuing to grow. But not at the pace that supports the VC math of a 10X return.

Therefore, they’re not going to be able to raise their next round of funding, and since they’re not self-sustaining with their cash flow, they’ll either be forced to sell to the hungry corp dev wolves or simply go out of business.

Not only will that consolidate the landscape through mass attrition, the large number of VC write-offs that will occur will make the space radioactive to investors, so far fewer martech start-ups will be able to to raise VC funding in the future. The engine of growth for the landscape will grind to a screeching halt.

Goodnight and good luck.

Martech VCs != Martech Vendors != Martech Customers

As with so many other predictions in this space, its most glaring flaw is that it’s a gross oversimplification. It’s next-most-glaring flaw is that it conflates that needs of large martech VCs with those of martech vendors and martech customers.

Now, as an empiricist, I agree that there are many funded martech companies that are not profitable today and are going to have a hard time raising large follow-on VC rounds because they can’t justify how they’ll deliver 10X returns at that scale on the timetable that institutional VCs have come to expect.

That said, I’m skeptical of pretty much every other assumption and inference around that martech apocalypse scenario.

The mother of all assumptions here is that you need large VC investment to grow a successful software company. Talk about an epic false dichotomy: either you can raise tens of millions (or hundreds of millions) and IPO to a billion dollar valuation, or you might as well not bother getting out of bed.

Those are the only companies that matter to large VCs with gargantuan funds that have to deploy at least $20 million or more in a portfolio company to make their economics work.

There will be some martech companies that fit that model. But doing the math on the total market, it’s obvious that there can’t be thousands of them.

But thinking that those are the only kind of software companies that matter to everyone else in the world — the only kind of software companies that can be successful and provide real value to their customers — is a Sand Hill Road fantasy from one or two decades ago.

It runs contrary to every other trend happening in software.

The Democratization of Software

So many big forces are democratizing the software business. On-demand cloud computing resources that continue to drop in price. An incredible array of open source software that lets any developer stand on the shoulders of giants — for free. The interoperability of APIs and microservices. Crowd sourced problem solving from expert communities around the globe. On-demand talent networks and dynamic group collaboration across any distance.

It is truly astounding the software that people can build without a lot of capital today.

A good friend of mine launched a software business a few years ago with a modest amount of angel funding, and through smart use of open source and Upwork-based talent has grown it into one of the leading vendors in their space. Organizations like the World Bank are their customers. They’re profitable, growing at a double-digit rate, expanding internationally, and innovating their industry in a myriad of remarkable ways.

A competitive venture not too long ago raised north of $20 million in funding — and blew it all with almost nothing to show for it in the end. Not even a viable product.

You might argue that stories like these are anomalies — and a couple of decades ago it might have been. But in the cloud era, I’d contend that this is likely to be a much more common path to success than the major VC route.

But don’t just take my word for it…

(Customer) Signal v. (VC) Noise

David Heinemeier Hansson, or DHH as he’s known by short-hand, is a co-founder and CTO of Basecamp (formerly 37signals), the creator of the immensely popular open source web application framework Ruby on Rails, the New York Times best-selling author of Rework and Remote, and a regular blogger on Medium under Basecamp’s publication Signal v. Noise.

Much of his recent writing on Medium is essentially antibiotics for the “must raise a lot of VC money” meme that has spread throughout the software start-up scene. Basecamp is Exhibit A for the alternative approach: a small, bootstrapped, yet highly profitable company, that customers love, and where employees love what they do (and don’t burn themselves out).

Here are a few of his greatest hits on this topic:

- RECONSIDER

- Resisting the lure of unicorn culture

- All or something

- Exponential growth devours and corrupts

- Don’t accelerate your startup

“Another anomaly!” you say? Basecamp is the Steve Jobs of non-VC software success?

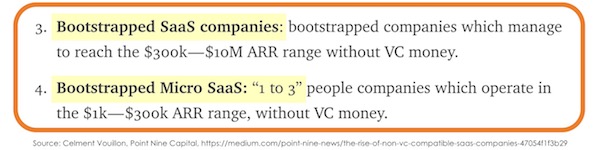

Then read The Rise of Non “VC compatible” SaaS Companies by Clement Vouillon, who actually works at a VC firm, Point Nine Capital.

“But surely all these small companies can’t compete against the giants?!” you might offer as a riposte. You need big companies with big funding to do big things, right?

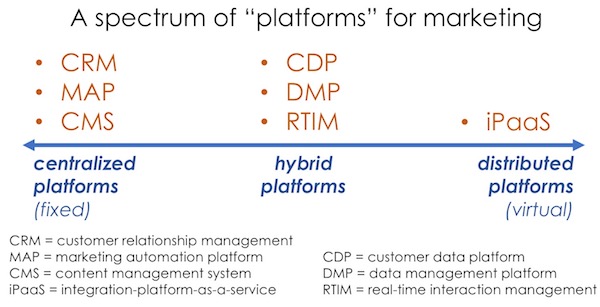

Not necessarily in a cloud-based software world. In addition to the economics of the democratization of software that we discussed above, increased “platformization” in the martech space is making it easier for more specialized solutions to plug into companies’ marketing stacks.

The average enterprises uses 91 marketing cloud services (a) because they can and (b) because it lets them tailor their toolset to their particular needs and wants. They don’t have to settle for what one or two major marketing clouds think is sufficient for everyone.

While you’re reading articles from folks who are much smarter about this stuff than I am, you should read 5 Ways to Compete With [Big] Incumbents by Steven Sinofsky.

Yes, Steven was the president of the Windows division at Microsoft and is now a board partner at the mega-VC firm Andreessen Horowitz. But his advice here is dead-on about how small, focused companies can deftly compete against the giants:

“Depth is your strength because your competitor is focused a checkbox or a tie, figuring out the internal organization dynamics of a response, or strategizing how to break from the corporate strategy. While you might be out-resourced you are also maniacally focused on delivering on a company-defining scenario or approach.”

Small, focused, passionate companies can make software that people really love.

There are more things in heaven and earth, Horatio

I’m not saying that there won’t still be great ventures in martech that will be able to successfully leverage large VC funding. I’m sure there will be.

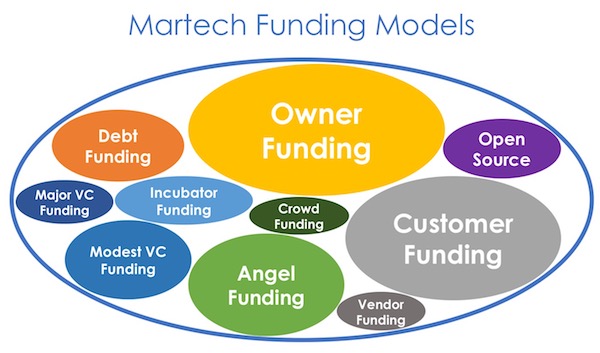

But there will be many more martech companies that can leverage more modest amounts of VC capital, angel funding, incubator funding, venture debt, crowdfunding, vendor funding, customer funding, open source community funding, or — making a business the old-fashioned way — by entrepreneurs launching it with sufficient funding from their own pockets.

One doesn’t preclude the other.

Keep in mind, the largest collection of companies in the marketing space are agencies (and related marketing services providers) — there are way more of them than martech companies — and almost none of them were funded by VCs. Yet there are many great, profitable firms there. And increasingly, more of them are getting into the software business too. (See above: The Democratization of Software.)

So going back to that set of unprofitable martech companies today who find themselves being squeezed out of the next round of their fundings. If they’ve got great products and great customers — and many of them do — I suspect there are more possible paths forward for them than just deal-or-die ultimatums.

Those other paths won’t necessarily be easy. They will almost certainly require them to significantly restructure their costs in order to become profitable. Some may have to explore more radical transformations, such as going open source. But those are options.

And as is the nature with any business, a number of them still won’t survive.

That may reduce the appetite for the kind of large VC investments in the martech space that we’ve seen over the past few years. But I don’t think it’s going to dampen the inventiveness of future martech entrepreneurs and the yearning for innovation from martech customers.

But again, I’m an empiricist, not a prognosticator. This is just my hypothesis. We’ll see how the data plays out in the years ahead.

What do you think will happen?

Get chiefmartec in your inbox

Join 42,000+ marketers and martech professionals who get my latest insights and analysis.