How big is the market for marketing software today?

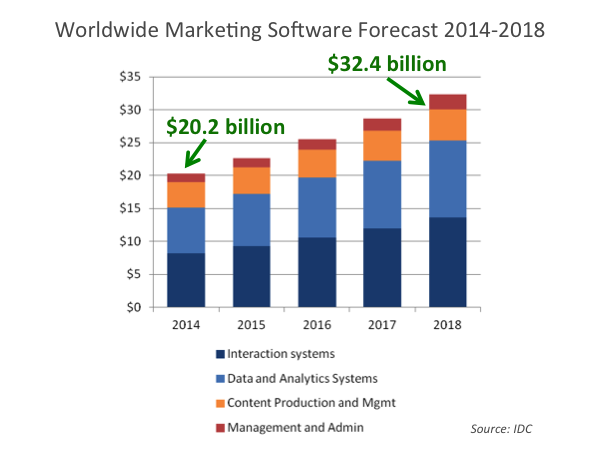

Gerry Murray at IDC has an answer to that question, which he announced in a blog post last week: $20.2 billion here in 2014. He expects that the market will have a compound annual growth rate (CAGR) of 12.4% for the next five years, resulting in a $32.4 billion market by 2018.

IDC breaks that market down into four broad categories:

- Interaction Systems — the majority of customer-facing marketing software advertising, digital commerce, marketing automation, web experience management, mobile apps, social media tools, etc.

- Content Production and Management — internal authoring and publishing tools, CMS platforms, DAM platforms, etc.

- Data and Analytics — storing data and producing insights from it, such as business intelligence, predictive analytics, financial analysis, and broader marketing analytics.

- Management and Administration — internal communications tools, workflows, budgeting, expense tracking, MRM, project management, collaboration tools, etc.

That’s just the software itself — although IDC predicts the rise of “marketing-as-a-service” (MaaS) offerings, through which agencies and other marketing service providers run the software on behalf of their clients, as part of a larger bundle of services. (I confess, I harbor some skepticism around the dynamics of agencies as the landlords of a brand’s marketing technology infrastructure — but that’s a topic for a whole different post. Either way, it won’t reduce the demand for the underlying software.)

The last time I saw a hard figure on this market was two years ago, with Dan Salmon’s estimate of $12.1 billion, which at the time represented 1% of global marketing spend.

If you take these numbers at face value, the marketing software market has grown by 67% in just two years — which when you’re starting with $12 billion as your baseline, that’s rather impressive.

But again, it’s still just a drop in the bucket in overall marketing spend. To put this in context, the most recent estimate of global advertising spend (just media purchases) from ZenithOptimedia is $523 billion in 2014. The spend on marketing software will be just 3.8% of what we spend on media this year.

However, the trend lines are certainly in software’s favor. Meanwhile, the advertising world is eyeball-to-eyball with a tremendous number of cataclysmic disruptions, such as:

- Print faded and TV advertising isn’t what it used to be (TiVo, HBO, Netflix, Amazon).

- Display advertising is a poor substitute (ad blockers, banner blindness, fraud, hate).

- Programmatic media buying is squeezing the margins of traditional agency cash cows.

- Data has forced greater transparency and performance-measured accountability.

- Search engines and social media thwart PR spin and inauthentic brand advertising.

Sorry, I keep drifting into wanting to write that post about the future of agencies. Soon enough. But my point in this article is simply that each one of those losses of territory in “advertising” stands to be replaced by other kinds of market engagements that are driven by software.

Put another way, I do think that $21.8 billion of venture investment in marketing technology is a pretty good bet.

IDC’s complete research report is available for purchase on their site.

Get chiefmartec in your inbox

Join 42,000+ marketers and martech professionals who get my latest insights and analysis.